March 2026 Mortgage Rates: Is It Time to Buy in Miami?

- By Miguel E. Hernandez

- Mar 10, 2026

Are mortgage rates going up or down in March 2026? Miguel E. Hernandez analyzes the 6.11% trend and how it impacts your Miami real estate investment.

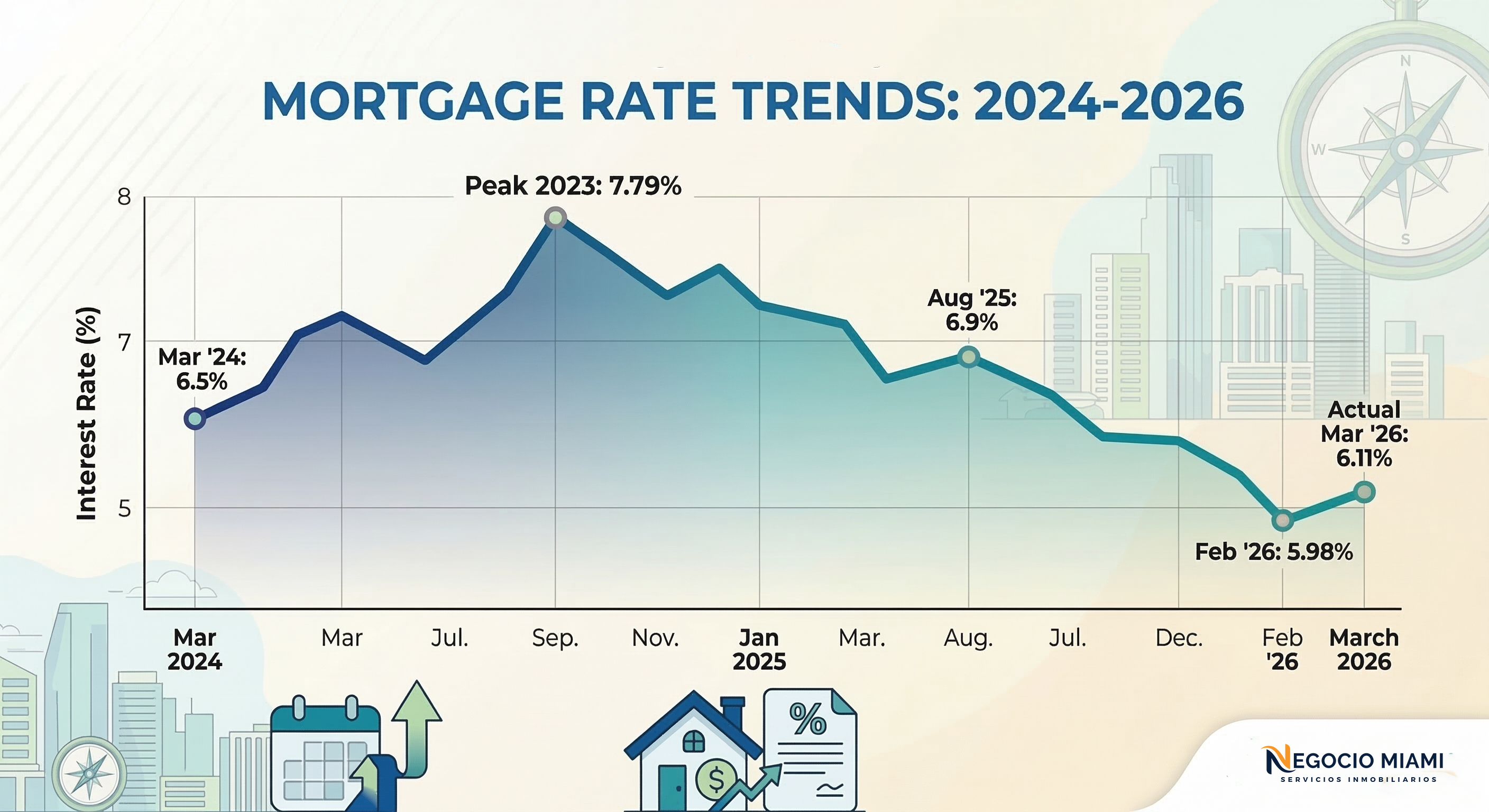

As a professional in the Florida real estate sector, I know that the single question dominating our coffee tables and Zoom meetings this month is: What is happening with mortgage rates in March 2026? After a hopeful close to February, the market has given us a small shake. Rates have risen slightly, settling at an average of 6.11% for 30-year loans, but before panic sets in, I want to analyze with you why this scenario remains a window of opportunity for those of us who know how to read between the lines.

Despite this daily adjustment, we remain firmly below the psychological barrier of 7% that worried us so much at the beginning of 2025. My goal today is to break down these numbers so you can make the smartest financial decision, whether you are looking for your first home or expanding your investment portfolio in South Florida.

The key in the Miami market is not waiting for rates to reach 3%, but understanding that the current 6%, combined with the area's equity growth, remains a solid business.Miguel E. Hernandez P.A.

Current State of Mortgage Rates in March 2026

To understand where we are going, we must see where we stand today, March 10, 2026. Volatility has been the constant, directly influenced by the yield of the 10-year Treasury bonds. Here is the current landscape of the products most requested by my clients:

| Loan Type | Current Average Rate | Weekly Trend |

|---|---|---|

| 30-Year Fixed | 6.11% | Slight rise |

| 15-Year Fixed | 5.53% | Stable |

| 20-Year Fixed | 6.05% | Stable |

| 10-Year Fixed | 5.68% | Slight decrease |

It is important to note that, although we see 6.11% today, we are coming from a recent historical low in the last week of February, when rates fell to 5.98%. If we compare this with the beginning of 2025, where we exceeded 7%, it is clear that the market is in a stabilization phase that is much more friendly for the buyer.

Why do rates fluctuate and what to expect from the FED?

Many of you ask me: "Miguel, is the FED going to lower rates this month?". The CME FedWatch tool indicates a 97% probability that rates will remain stable at the March meeting. The Federal Reserve is being cautious following the three cuts we saw at the end of 2025.

This stability, although it may seem boring, is positive. It prevents aggressive speculation and allows serious buyers to get pre-qualified with real numbers and not based on assumptions.

- Treasury Bonds: Their downward trend presages marginal drops in mortgages.

- Inflation: It remains the enemy to beat to see rates below 5.5%.

- Inventory: In Miami, demand remains high, which compensates for the cost of money.

Historical Analysis: A Necessary Perspective

To keep our composure, let's look in the rearview mirror. In 2023, we saw rates of 7.79%. If we go further back, in the 80s, rates exceeded 16%. The 6% of these March 2026 mortgage rates is, in historical terms, a healthy equilibrium point.

Since mid-2025, the general trend has been downward. Fannie Mae projects that by the second quarter of this year we will stabilize at 6.0%. My personal recommendation is that if you find the ideal property in our exclusive developments, do not wait for a miraculous drop that may never arrive.

How to choose the right mortgage for your profile

Not all mortgages are the same. The choice depends on your cash flow and your long-term plans. Let's look at a practical exercise for a $350,000 loan:

- Conservative Option (30 years at 6.23%): Monthly payment of $2,150. Ideal for maintaining monthly liquidity.

- Aggressive Option (15 years at 5.63%): Monthly payment of $2,883. You save over $250,000 in total interest.

- Hybrid Strategy: Take the 30-year loan for security, but make additional payments to the principal when your finances allow.

Remember that factors such as your credit score and the down payment are decisive. A 20% down payment not only eliminates private mortgage insurance but usually guarantees you a better rate.

Frequently Asked Questions (FAQ)

1. Is it better to buy now or wait until the end of 2026?

Waiting can be risky. If rates lower further, competition for properties for sale will increase, which will likely drive up property prices, canceling out the rate savings.

2. Can I refinance if rates drop to 5% next year?

Of course! It is a common strategy. "Marry the house, date the rate." You secure the property today and refinance when the market improves.

3. What documents do I need to take advantage of these rates?

The main thing is to demonstrate income stability, a clean credit report, and verifiable funds for closing. I invite you to speak with me directly to review your case.

Conclusion: Your future in Miami starts today

The March 2026 mortgage rates show us a mature and stable market. With an average of 6.11%, the dream of owning a property in Florida is fully attainable and financially logical. Do not let small daily fluctuations distract you from the final goal: building wealth in one of the fastest-growing cities in the world.

I am here to advise you every step of the way, from pre-qualification to key delivery. Let's make your investment in Miami happen!